The past two years have seen auto retailers adapt to limited vehicle inventory and pandemic restrictions while driving profits to new heights. Now dealers face rising interest rates — a critical concern for an industry that relies on capital to fund operations and growth. For some, it’s time for a balance sheet review and risk management reset.

Changing Conditions Dealers Must Watch

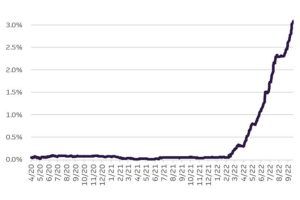

The Fed (Federal Reserve) has already taken aggressive steps by raising rates to throttle persistent inflationary pressure in the U.S. In the past year, we’ve seen the Fed hike the short-term rate by 3.00% (300 basis points). But with low inventory and reduced need for floor plan loans, many dealers haven’t yet felt the full impact of rising rates.

1-month CME Term SOFR since the beginning of the pandemic

As you imagine what’s next for the economy and your dealership, the impact of rising rates comes into sharper focus. For instance, if vehicle supply and demand start to realign, higher inventory levels could mean more floor plan loans on balance sheets.

As you look at business assets, the recent surge in inflation strengthening real estate values could provide an additional source of funds that you can tap into if needed. Unfortunately, when it comes to expansion and new construction, inflation will cut the other way by driving up building costs and the loans needed to finance them.

Sustained volatility in economic and market conditions makes planning for these possibilities and others both challenging and critical. Your risk management planning needs to focus on balance sheet moves available to you today — options that may be closed off tomorrow — to protect your dealership from economic and rate volatility and keep your cost of capital low.

Actions To Get Ahead

As economic and market conditions are shifting, you’ll want to ground your capital decisions in your business plans for your dealership and your personal goals as an owner. You can walk through a few steps — on your own or with your banker — to gauge the impact that rising rates will have on your business and identify actions you can take to mitigate their effect.

Step 1 — Start with your goals and plans: Balance sheet risk management starts by asking, “Where will my business be in five years?” Your goals might lead you to look for funds to grow, seek ways to release capital to equity holders or lenders, or explore other restructuring moves that might accomplish a bit of both.

Timing of those capital flows matters, and your options may look very different if you’re planning to exit the business versus being committed for the long haul.

Step 2 — Evaluate funding flows: Look at where you need funds, where you have them, and what sources (and especially at what cost) you can tap into to find capital. What happens to your cost of capital and valuation as rates rise? Where do you have needs in the future that will likely have to be met with additional, higher-cost capital? Have you considered ways to manage cash more strategically now that effective liquidity management can yield elevated returns?

Step 3 — Envision what the future looks like for your dealership: Add the dynamics that you expect will change over the coming years. When do you think floor plan inventory will return to normal levels? One year? Two years? Potentially a longer time frame? What do higher construction costs mean for your dealership? Will the economy cool before you have to undertake your next building project? What changes will the ongoing electrification of vehicles and any regulatory shifts bring to your dealership?

Step 4 — Get specific about actions you should take: When you’re protecting yourself in a rising rate environment, your primary move is to raise capital earlier when rates are lower and consider financial instruments like swaps as insurance. It doesn’t make sense for all situations, but commercial real estate and blue-sky loans are often amenable to this strategy.

As you’re thinking about what works for your business, some of the strategies below might fit your situation:

- If you expect inventory to return to more normal levels but want to protect your business from the risk of higher floating rates, you could target more liquidity to cushion against increased interest expense on floor plan lines. Or, to protect your bottom line, consider fixing rates on other outstanding loans that may currently be variable and subject to future rate hikes.

- If you want more cash to invest in growth or to be ready for whatever comes next, you can secure loans now. Consider a cash-out commercial mortgage that, if fixed, could protect you from higher interest rates down the road and give you funds for capital expenditures like renovations or preparing for the shift to EVs. If rates continue to climb, you’ll have the peace of mind of having funds at a lower cost to cover future uncertainty. (Don’t forget that the cash-out proceeds from the loan can be earning interest all along.)

- If you need cash for family/shareholder dividends or to finance a transition or succession, think about a dividend recap, particularly if you need liquidity now while you’re continuing to make moves that could help your dealership draw a higher valuation in the future. Or, as mentioned before, you could tap into increased real estate values to provide these proceeds.

- If you expect inventory to return to more normal levels but want to protect your business from the risk of higher floating rates, you could target more liquidity to cushion against increased interest expense on floor plan lines. Or, to protect your bottom line, consider fixing rates on other outstanding loans that may currently be variable and subject to future rate hikes.

Step 5 — Look at all elements of financial risk: Interest rates may be front and center, but a comprehensive approach to financial risk needs to look beyond the cost of capital. Cyberfraud threats and weather events, along with business property, lot inventory, and liability exposure, can have a devastating effect on a thriving dealership. Insurance can protect you from events that can put your dealership at financial risk — talk to Truist’s McGriff Insurance to see how we can help.

Preparing your dealership for a range of financial possibilities should be a priority for you and your financial advisors. With a rising rate environment, now’s the time to talk to your Truist Dealer Services relationship manager about a balance sheet risk management review.

Have You Taken Measures To Keep Your Cost Of Capital Low While Rates Rise?

Preparing your dealership for a range of financial possibilities should be a priority for you and your financial advisors. With a rising rate environment, now’s the time to talk to your Truist Dealer Services relationship manager about a balance sheet risk management review.